Kelly Criterion for Casino Games: When Math Tells You to Sit Out

Most betting systems answer the wrong question. They tell you how to chase losses or press wins, but they never address the only number that actually matters: how much of your bankroll should ride on a single wager. The Kelly criterion does. It is a formula from 1956, written by a Bell Labs physicist named John Kelly, and it gives a precise stake size that maximizes the long-run growth of your money. The brutal part, and the part nobody at the casino wants you to know, is that for almost every game on the floor, the Kelly criterion casino answer is a flat zero. Bet nothing. Walk away. That isn’t a slogan — it’s what the algebra says.

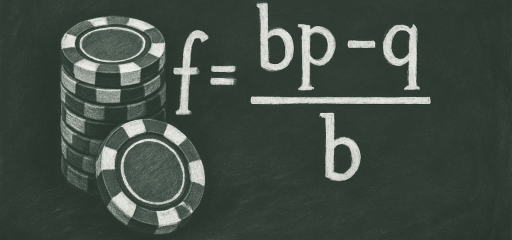

The Kelly formula in one line

Here is the whole thing:

f* = (bp − q) / b

That is it. No tables, no proprietary system, no subscription. f* is the fraction of your bankroll you should wager. b is the net odds on the bet (a $1 win on a $1 stake means b = 1; a payout of $5 profit on $2 staked means b = 2.5). p is the probability you win. q is the probability you lose, which is just 1 − p. Plug in, divide, and you get a number between negative and positive one. That number is the share of your bankroll the math says to put down.

What each variable is actually doing

The numerator, bp − q, is the expected value of a $1 bet. If it is positive, the wager has an edge. If it is negative, it does not. Dividing by b scales the bet to account for the payout ratio. A bet that wins rarely but pays huge deserves a different stake than a coin flip with a small edge, even if their expected values match.

That structure is what makes Kelly different from flat betting. It cares about two things at once: how often you win, and how much you win when you do. A 51% edge on an even-money bet and a 6% edge on a 10-to-1 longshot do not deserve the same fraction of your roll.

The brutal answer for the casino floor

Roulette, baccarat, craps, slots, keno, sic bo, the side bets at blackjack — every one of these games has a built-in house edge. That means p, the probability of winning, is lower than what the payout implies it should be. Run the numbers through Kelly and bp − q comes out negative. Divide a negative number by a positive b, and f* is negative.

A negative Kelly fraction has a literal interpretation: bet the other side. If that is not possible, which it almost never is at a casino, the next-best Kelly answer is f* = 0. Wager nothing. Keep your money in your pocket. The formula isn’t being polite about it — it’s telling you that any positive stake on a negative-edge game shrinks your bankroll over time, faster the more you bet.

A worked example: the baccarat banker bet

The banker bet in baccarat is often praised as one of the “best” wagers in the casino because the house edge is only about 1.06%. Let’s run it through Kelly honestly.

The banker wins roughly 45.86% of resolved hands, loses 44.62%, and ties 9.52% (ties push). Setting ties aside, the conditional win probability is about p = 0.5068. The payout is even money minus a 5% commission, so b = 0.95. Then q = 1 − p = 0.4932.

f* = (0.95 × 0.5068 − 0.4932) / 0.95 = (0.4815 − 0.4932) / 0.95 = −0.0123.

Kelly says stake −1.23% of your bankroll on the banker bet. You cannot do that. The casino does not offer the other side at fair terms. So the operational answer is zero. The “best bet in the casino” still fails the Kelly test. That is not a knock on baccarat; it is the math being consistent.

When Kelly actually says yes

The formula starts handing out positive numbers when you have a real edge. That is the world of advantage play, and it is a narrow world:

- Card-counted blackjack. A skilled counter playing favorable rules and spreading bets can pull a long-run edge in the neighborhood of 0.5% to 1.5%.

- Live poker against weaker opponents. The house rakes the pot, but if your skill edge over the table exceeds the rake, your expectation is positive.

- Biased or trackable roulette wheels. Rare today, but historically real. Visual ballistics and wheel-bias work have produced documented edges.

- Sports betting at soft lines. Beating closing prices by even a percent or two before the books adjust is a measurable edge.

- Video poker with promotions or comps. A few specific paytables, combined with cashback or mailers, can flip the expected return above 100%.

For a counted blackjack edge of +1% at roughly 1-to-1 payoff, plug in p ≈ 0.505 and b ≈ 1. Then f* ≈ (1)(0.505) − 0.495 = 0.01. About 1% of bankroll per hand. For a sports bet at -110 odds (b = 10/11 ≈ 0.909) with a +3% edge, the Kelly fraction works out to roughly 3% × (11/10) ≈ 3.3% of bankroll. Modest numbers, even with a real edge.

Kelly fractions for different edges and odds

The table below shows full-Kelly stakes for a range of edges and payouts. It assumes the edge is your real, honest, long-run edge, not what you hope it is.

| Edge | Even money (b = 1) | -110 (b ≈ 0.909) | +150 (b = 1.5) | 5-to-1 (b = 5) |

|---|---|---|---|---|

| +0.5% | 0.5% | 0.55% | 0.33% | 0.10% |

| +1% | 1.0% | 1.10% | 0.67% | 0.20% |

| +2% | 2.0% | 2.20% | 1.33% | 0.40% |

| +3% | 3.0% | 3.30% | 2.00% | 0.60% |

| +5% | 5.0% | 5.50% | 3.33% | 1.00% |

| +10% | 10.0% | 11.0% | 6.67% | 2.00% |

| Negative | 0% (sit out) | 0% (sit out) | 0% (sit out) | 0% (sit out) |

Notice how thin the stakes are even at a 3% edge. Notice how longshot payouts shrink the recommended fraction. And notice the bottom row, which covers everything you can bet on a casino floor that is not advantage play.

Fractional Kelly: half, quarter, and why pros use them

Full Kelly is mathematically optimal for one thing: the long-run growth rate of your bankroll, assuming you know p and b exactly. In the real world, you do not. Your edge is an estimate. Your win probability is a model output, not a fact. Overbet your estimate and the swings can wipe you out before the long run gets around to vindicating you.

So practitioners scale down. Half-Kelly bets half of f*, quarter-Kelly bets a quarter. The trade-off is well known and surprisingly favorable: half-Kelly gives up only about 25% of the long-run growth rate but cuts the variance of bankroll swings by roughly 75%. Quarter-Kelly gives up around 44% of growth and cuts variance by about 94%. For most working advantage players, half-Kelly is the practical default.

Why even +EV players bet fractionally

Three reasons keep coming up:

- Edge estimation error. If you think you have a 2% edge and actually have 1%, full Kelly is overbetting by 100%. Half-Kelly survives that mistake; full Kelly does not.

- Drawdown tolerance. A full-Kelly bettor with a real edge still faces a meaningful chance of losing half their bankroll at some point. Most humans do not handle that well, and emotional decisions destroy more bankrolls than bad math.

- Compounding penalties. Bet-sizing errors compound geometrically. Two units of edge overestimate plus one unit of variance underestimate is more damaging than the sum of the parts.

Fractional Kelly is the price you pay for not knowing the universe exactly. It is cheap insurance.

The most common Kelly mistake

The mistake isn’t in the formula — it’s in the input. People overestimate their edge, and Kelly faithfully multiplies that overestimate into a too-large stake. The counter who thinks they are running +1% but is actually playing through a shaky shuffle at +0.2% is overbetting by a factor of five. The sports bettor who treats their gut as a 3% edge when their closing-line value says 0.5% is in the same trap.

A second common error is treating short-term results as evidence of edge. Win ten coin-flips in a row and Kelly will not care; the formula needs the true p, not the observed one. Without a model — counting system, line-shopping discipline, documented bias — you do not have a p, you have a guess. Kelly is unforgiving to guesses. A third error is ignoring the cost side of the game: rake, vig, commissions, and tipping all eat into b before you ever sit down. A poker game that looks juicy at face value can have an effective Kelly fraction of zero once a 5% rake and a $5 hourly tip are baked in. Run those costs through the formula honestly, and a surprising number of “beatable” spots turn out to be break-even at best.

Finally, Kelly assumes you can resize every bet to your current bankroll. In practice, table minimums, betting limits, and the granularity of chips force rounding. When the math says bet $2.30, you cannot. Round down rather than up, and the long-run penalty is small. Round up out of habit, and you are quietly running an over-Kelly strategy without realizing it.

If you want a sanity check, work through the probability foundations in this MIT OpenCourseWare probability and statistics course, and read the betting-system breakdowns at Wizard of Odds. Both will reset your expectations of what a real, measurable edge looks like.

For more on the algebra and worked numerical examples behind formulas like Kelly, the explainers at Effortless Math are a clean place to start.

Frequently asked questions

Does Kelly guarantee I will make money?

No. Kelly maximizes the long-run growth rate of your bankroll given a real edge. With no edge, it tells you to bet nothing, and that is the most honest financial advice in gambling. With an edge, it still allows large short-term swings.

Why does Kelly say to bet zero on every casino game?

Because the house edge makes bp − q negative. The formula does not care about entertainment value or how much fun you are having. It only computes growth-optimal stake sizes, and a negative-edge bet has no growth-optimal positive stake.

Can I use Kelly for a parlay or longshot?

You can, and the formula will punish you for it. As b grows, f* shrinks for the same edge. A real 5% edge on a 10-to-1 longshot is a smaller bankroll fraction than a 5% edge on an even-money wager, because the variance is higher.

Is half-Kelly really worth giving up growth?

For almost everyone, yes. Cutting variance by 75% while only giving up 25% of growth is one of the best risk-adjusted trades in finance, let alone in gambling. The people who can stomach full Kelly are rarer than they think.

What if I do not know my exact edge?

Then you do not know your exact Kelly. Use a conservative estimate, divide by two or four, and treat the result as a ceiling, not a target. The smaller your sample of past results, the more aggressively you should scale down.

Gambling outcomes are uncertain; no strategy guarantees profit.

Related to This Article

More math articles

- Words for Agreement, Conflict, Power, and Law

- Riemann Sum Calculator (Left, Right, Midpoint, Trapezoid)

- Math Tools That Help Students Organize Research Data

- Grade 6 Math: Area of Composite Figures

- How to Solve Prime Factorization with Exponents?

- 5th Grade IAR Math FREE Sample Practice Questions

- Area for 5th Grade: Squares, Rectangles, and Composite Figures

- How to Sketch Trigonometric Graphs?

- The Missouri MAP Grade 3 Math Worksheet Set — 49 Free Printable PDFs

- How to Decode the Definite Integral

What people say about "Kelly Criterion for Casino Games: When Math Tells You to Sit Out - Effortless Math"?

No one replied yet.