How to Understand Cost of Credit and Loans? (+FREE Worksheet!)

When you borrow money—whether through a credit card, a car loan, or a student loan—the lender charges you extra for the privilege of using their money. That extra charge is called interest, and it can turn a seemingly affordable purchase into something much more expensive. Understanding the cost of credit and loans is one of the most important financial skills an 8th grader can develop.

Think of interest as a rental fee: you are renting someone else’s money, and the longer you keep it, the more rent you pay. Two key factors determine how much interest you owe—the interest rate and the loan term (how many years you borrow for). A higher rate or a longer term always means more interest paid overall.

Key Formulas for Credit and Loans

Most loan calculations in 8th-grade math use one of two formulas:

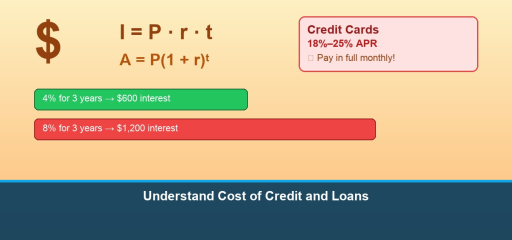

- Simple Interest: \(I = P \cdot r \cdot t\), where \(P\) is the principal (amount borrowed), \(r\) is the annual interest rate (as a decimal), and \(t\) is the time in years.

- Compound Interest: \(A = P(1 + r)^t\), where \(A\) is the total amount owed after \(t\) years.

- Total Repayment: Principal + Total Interest

Simple interest grows at a constant rate—the same dollar amount each year. Compound interest charges interest on top of previously accumulated interest, so the balance grows faster over time. Credit cards almost always use compound interest, which is why unpaid balances can snowball quickly.

How Interest Rate and Loan Length Affect Cost

Consider borrowing \(\$5{,}000\). At 4% simple interest for 3 years, the interest is \(5{,}000 \times 0.04 \times 3 = \$600\). But at 8% for 3 years, the interest doubles to \(\$1{,}200\). Doubling the rate doubles the cost.

Now look at loan length: \(\$4{,}000\) at 5% for 3 years costs \(4{,}000 \times 0.05 \times 3 = \$600\) in interest. Stretch that to 5 years and the interest jumps to \(4{,}000 \times 0.05 \times 5 = \$1{,}000\). The longer loan costs \(\$400\) more even at the same rate.

Comparing Loan Types

| Loan Type | Typical Rate | Key Risk |

|---|---|---|

| Bank personal loan | 6%–12% | Moderate cost |

| Credit card | 18%–25% | Very high interest if not paid in full |

| Payday / easy-access loan | 300%–400%+ | Extreme cost, debt trap |

| Student loan (federal) | 4%–7% | Lower rate, long repayment |

Step-by-Step Examples

Example 1 — Simple Interest: Short vs. Long Loan

Compare borrowing \(\$4{,}000\) at 5% simple interest for 3 years versus 5 years.

Solution:

- 3-year interest: \(I = 4{,}000 \times 0.05 \times 3 = \$600\). Total repaid: \(\$4{,}600\).

- 5-year interest: \(I = 4{,}000 \times 0.05 \times 5 = \$1{,}000\). Total repaid: \(\$5{,}000\).

The longer loan costs \(\$400\) more in interest.

Example 2 — Compound Interest on a Credit Card

You charge \(\$800\) on a credit card at 20% annual compound interest and make no payments for 2 years. How much do you owe?

Solution: \(A = 800(1.20)^2 = 800 \times 1.44 = \$1{,}152\).

You owe \(\$352\) extra in interest alone.

Example 3 — Comparing Two Interest Rates

Borrow \(\$2{,}000\) for 4 years. Bank A charges 6% simple; Bank B charges 10% simple.

Solution:

- Bank A: \(I = 2{,}000 \times 0.06 \times 4 = \$480\). Total: \(\$2{,}480\).

- Bank B: \(I = 2{,}000 \times 0.10 \times 4 = \$800\). Total: \(\$2{,}800\).

A 4-percentage-point higher rate costs an extra \(\$320\).

Video Lesson

Watch this video for additional examples and a step-by-step walkthrough:

Practice Problems

- \(P = \$3{,}000\), \(r = 5\%\), \(t = 2\) years. Find the total repayment (simple interest).

- \(P = \$3{,}000\), \(r = 5\%\), \(t = 5\) years. Find the total repayment.

- \(P = \$5{,}000\), \(r = 4\%\), \(t = 3\) years. Find the interest.

- \(P = \$5{,}000\), \(r = 8\%\), \(t = 3\) years. Find the interest.

- \(P = \$1{,}500\), \(r = 18\%\), \(t = 1\) year. Find the total repayment.

- \(P = \$1{,}500\), \(r = 6\%\), \(t = 1\) year. Find the total repayment.

- \(P = \$600\), \(r = 20\%\) compound, \(t = 2\) years. Find \(A\).

- \(P = \$600\), \(r = 20\%\) simple, \(t = 2\) years. Find the total.

- Marcus borrows \(\$6{,}000\) for a car. Bank A offers 5% simple for 3 years; Bank B offers 4% simple for 5 years. Which costs less total interest?

- Layla puts \(\$500\) on a credit card at 24% compound interest and makes no payments for 3 years. How much does she owe?

Solutions

- \(I = 3{,}000 \times 0.05 \times 2 = \$300\). Total = \(\$3{,}300\).

- \(I = 3{,}000 \times 0.05 \times 5 = \$750\). Total = \(\$3{,}750\). Three extra years cost \(\$450\) more.

- \(I = 5{,}000 \times 0.04 \times 3 = \$600\).

- \(I = 5{,}000 \times 0.08 \times 3 = \$1{,}200\). Double the rate doubles the interest.

- \(I = 1{,}500 \times 0.18 \times 1 = \$270\). Total = \(\$1{,}770\).

- \(I = 1{,}500 \times 0.06 \times 1 = \$90\). Total = \(\$1{,}590\). Lower rate saves \(\$180\).

- \(A = 600(1.20)^2 = 600 \times 1.44 = \$864\).

- \(I = 600 \times 0.20 \times 2 = \$240\). Total = \(\$840\). Compound cost \(\$24\) more.

- Bank A interest: \(6{,}000 \times 0.05 \times 3 = \$900\). Bank B interest: \(6{,}000 \times 0.04 \times 5 = \$1{,}200\). Bank A costs \(\$300\) less.

- \(A = 500(1.24)^3 \approx 500 \times 1.9066 = \$953.31\). She owes about \(\$953\); roughly \(\$453\) is interest.

Real-World Applications

Car Loans: A \(\$10{,}000\) car loan at 6% simple interest for 5 years costs \(\$3{,}000\) in interest—bringing the true price to \(\$13{,}000\). Monthly payments would be about \(\$216.67\).

Credit Card Minimum Payments: Paying only the minimum on a \(\$2{,}000\) balance at 18% can result in over \(\$3{,}000\) in total interest and take more than 8 years to pay off. Always pay more than the minimum!

Common Mistakes to Avoid

- Focusing only on the monthly payment. A lower monthly payment over a longer term often costs much more in total interest.

- Forgetting that compound interest grows on itself. A 20% compound rate costs more than 20% simple over the same period.

- Ignoring payday-loan rates. Rates above 300% can turn a small loan into a massive debt trap.

Study Tips

- Always calculate total interest paid, not just whether you can afford the monthly payment.

- Credit cards charge interest on the unpaid balance. Paying the full balance each month means \(\$0\) in interest.

- The golden rule: Borrow as little as possible, at the lowest rate, for the shortest time.

Frequently Asked Questions

What is the difference between simple and compound interest?

Simple interest is calculated only on the original principal: \(I = Prt\). Compound interest is calculated on the principal plus any interest already earned, so it grows faster: \(A = P(1+r)^t\).

Why are credit card rates so high?

Credit cards are unsecured debt—there is no collateral backing the loan. The lender takes on more risk, so they charge a higher rate (often 18%–25%) compared to secured loans like car loans or mortgages.

How can I reduce the total cost of a loan?

Three strategies: (1) borrow a smaller amount, (2) find a lower interest rate, and (3) pay it off as quickly as possible. Making extra payments toward the principal also helps reduce compound interest.

Related to This Article

More math articles

- How to Factor Numbers? (+FREE Worksheet!)

- 7th Grade Wisconsin Forward Math Worksheets: FREE & Printable

- Subject-Verb Agreement

- A Comprehensive Collection of Free CBEST Math Practice Tests

- Relating Fractions and Decimals for 4th Grade

- CLEP College Algebra Worksheets: FREE & Printable

- SSAT Middle Level Math FREE Sample Practice Questions

- 7th Grade K-PREP Math Worksheets: FREE & Printable

- Top 10 Tips You MUST Know to Retake the TASC Math

- How to Support Grade 8 Reading at Home: 12 Smart Strategies That Build Independence

What people say about "How to Understand Cost of Credit and Loans? (+FREE Worksheet!) - Effortless Math"?

No one replied yet.