How to Plan and Save for College? (+FREE Worksheet!)

College is one of the biggest investments a person can make—and one of the most expensive. A two-year community college and a four-year university have very different price tags, and the total cost of attendance goes far beyond tuition. It includes fees, room and board, books, supplies, and personal expenses. The earlier you start saving, the more time your money has to grow through compound interest. Even setting aside a small amount each month in 8th grade can add up to something significant by the time you graduate high school.

In this guide, we will break down the true cost of college, show you how to calculate savings goals, explore the power of compound interest for building a college fund, and give you practice problems with full solutions so you can plan confidently for your future.

Understanding the Total Cost of College

Many people think of “college cost” as just tuition. In reality, the Total Cost of Attendance (COA) includes several components:

| Cost Component | 2-Year College (Annual) | 4-Year Public University (Annual) |

|---|---|---|

| Tuition & Fees | ≈ \(\$4{,}000\) | ≈ \(\$11{,}000\) |

| Room & Board | ≈ \(\$9{,}000\) | ≈ \(\$12{,}000\) |

| Books & Supplies | ≈ \(\$1{,}400\) | ≈ \(\$1{,}200\) |

| Personal / Transport | ≈ \(\$3{,}000\) | ≈ \(\$3{,}000\) |

| Total per Year | ≈ \(\$17{,}400\) | ≈ \(\$27{,}200\) |

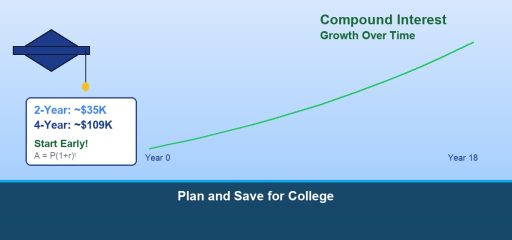

| Total (All Years) | ≈ \(\$34{,}800\) | ≈ \(\$108{,}800\) |

The gap between a 2-year and 4-year school is substantial—over \(\$74{,}000\) in total. That is why many students start at a community college and transfer to a university to save money.

Key Formulas for College Savings

- Monthly savings (no interest): \(\text{Monthly savings} = \dfrac{\text{Amount needed}}{\text{Number of months}}\)

- Compound interest growth: \(A = P(1 + r)^t\)

- Future cost with inflation: \(A = \text{Present cost} \times (1 + \text{inflation rate})^t\)

Compound interest is your best friend when saving. If you deposit money into an account that earns interest, you earn interest not only on your original deposit but also on the interest you have already earned. Over many years, this creates a snowball effect.

Step-by-Step Examples

Example 1 — Calculating Student Savings Needed

A 2-year community college costs \(\$3{,}800\)/year in tuition, \(\$1{,}200\)/year for books, and \(\$2{,}500\)/year for transportation. The family pays 60%. How much must the student save?

Solution:

- Annual cost: \(3{,}800 + 1{,}200 + 2{,}500 = \$7{,}500\)

- 2-year total: \(7{,}500 \times 2 = \$15{,}000\)

- Family pays: \(15{,}000 \times 0.60 = \$9{,}000\)

- Student must save: \(15{,}000 – 9{,}000 = \$6{,}000\)

Example 2 — Monthly Savings Plan

An 8th grader has 5 years until college and needs to save \(\$6{,}000\) (ignoring interest). How much per month?

Solution: \(5 \text{ years} = 60 \text{ months}\). Monthly savings: \(\dfrac{6{,}000}{60} = \$100\) per month.

Example 3 — The Power of Starting Early

A family deposits \(\$3{,}000\) at a child’s birth into an account earning 5% compound interest. How much is it worth at age 18? What if they waited until age 8?

Solution:

- At birth (18 years): \(A = 3{,}000(1.05)^{18} \approx 3{,}000 \times 2.4066 = \$7{,}220\)

- At age 8 (10 years): \(A = 3{,}000(1.05)^{10} \approx 3{,}000 \times 1.6289 = \$4{,}887\)

Starting at birth earns approximately \(\$2{,}333\) more—that is the power of compound interest over time.

Video Lesson

Watch this video for additional examples and a step-by-step walkthrough:

Practice Problems

- A 2-year community college charges \(\$4{,}200\)/year tuition, \(\$1{,}300\)/year books, and \(\$2{,}800\)/year transport. What is the total cost for both years?

- A 4-year university costs \(\$28{,}000\) per year. What is the total cost for all four years?

- First-year college cost is \(\$25{,}000\). A family contributes \(\$15{,}000\). How much must the student cover?

- A student needs to save \(\$10{,}000\) in 4 years with no interest. How much per month?

- You save \(\$75\) per month for 5 years at 0% interest. How much do you have?

- You deposit \(\$2{,}000\) at 4% compound interest for 5 years. What is the total?

- A 2-year college costs \(\$36{,}000\) total and a 4-year university costs \(\$112{,}000\) total. What is the difference?

- A family contributes 45% of a \(\$30{,}000\) first-year cost. How much does the family pay? How much does the student need?

- You save \(\$150\) per month. How many months to reach \(\$9{,}000\)?

- A school costs \(\$25{,}000\)/year today. If costs rise 3% per year, what will one year cost in 5 years?

Solutions

- Annual: \(4{,}200 + 1{,}300 + 2{,}800 = \$8{,}300\). Total: \(8{,}300 \times 2 = \$16{,}600\).

- \(28{,}000 \times 4 = \$112{,}000\).

- \(25{,}000 – 15{,}000 = \$10{,}000\).

- \(4 \text{ years} = 48 \text{ months}\). \(10{,}000 \div 48 \approx \$208\) per month.

- \(75 \times 60 = \$4{,}500\).

- \(A = 2{,}000(1.04)^5 \approx 2{,}000 \times 1.2167 = \$2{,}433\).

- \(112{,}000 – 36{,}000 = \$76{,}000\).

- Family pays: \(30{,}000 \times 0.45 = \$13{,}500\). Student needs: \(30{,}000 – 13{,}500 = \$16{,}500\).

- \(9{,}000 \div 150 = 60\) months (5 years).

- \(A = 25{,}000(1.03)^5 \approx 25{,}000 \times 1.1593 = \$28{,}982\).

Scholarships and Financial Aid

Scholarships and grants are “free money”—you do not have to pay them back. Always search for them!

- Scholarship A pays \(\$5{,}000\)/year for 4 years = \(\$20{,}000\) total.

- Scholarship B pays \(\$18{,}000\) as a one-time award.

- Scholarship A has a greater total value. However, Scholarship B provides a large lump sum upfront, which can cover first-year tuition, a housing deposit, and supplies when costs are highest.

A 529 savings plan is a special investment account designed for education expenses. It grows tax-free, but be aware of fees. For example, a 529 plan with a 0.5% annual fee on \(\$10{,}000\) earning 6% before fees yields an effective rate of 5.5%. After 10 years: \(10{,}000(1.055)^{10} \approx \$17{,}081\). Without fees it would be \(\$17{,}908\)—the fees cost about \(\$827\) over a decade.

Real-World Applications

Starting Early Pays Off: Saving just \(\$50\)/month at 5% interest for 10 years grows to approximately \(\$7{,}764\)—much more than \(50 \times 120 = \$6{,}000\) without interest. That extra \(\$1{,}764\) is free money from compound interest.

Inflation Matters: College costs rise about 3%–5% per year. A school that costs \(\$25{,}000\) today could cost nearly \(\$29{,}000\) in just 5 years. Planning ahead means accounting for future prices, not just today’s.

Common Mistakes to Avoid

- Only counting tuition. Room and board, books, and personal expenses can easily double the sticker price.

- Waiting too long to save. Starting in 12th grade gives you 1 year of growth. Starting in 8th grade gives you 4–5 years. Compound interest rewards early savers.

- Ignoring inflation. Today’s costs will be higher by the time you enroll. Use the future-cost formula to plan accurately.

- Forgetting scholarships. Many scholarships go unclaimed each year. Apply early and often.

Study Tips

- Total Cost of Attendance = Tuition + Fees + Room & Board + Books + Personal Expenses.

- Start saving early—even small monthly amounts add up significantly with compound interest.

- Compare 2-year and 4-year options. Starting at a community college and transferring can save tens of thousands of dollars.

- Scholarships and grants reduce the amount you need to borrow. Treat scholarship applications like a part-time job.

Frequently Asked Questions

How much does college really cost?

It depends on the school type. A 2-year community college runs about \(\$17{,}000\)–\(\$18{,}000\) per year (total cost of attendance), while a 4-year public university averages about \(\$27{,}000\) per year. Private universities can cost \(\$50{,}000\)+ per year.

Is it too early to start saving in 8th grade?

Absolutely not—it is actually the perfect time. You have 4–5 years before college, which gives compound interest time to grow your savings. Even \(\$50\)–\(\$100\) per month makes a real difference.

What is a 529 plan?

A 529 plan is a tax-advantaged savings account specifically designed for education expenses. The money grows tax-free as long as it is used for qualified education costs like tuition, room and board, and books.

Related to This Article

More math articles

- 10 Most Common ATI TEAS 7 Math Questions

- Intelligent Math Puzzle – Challenge 85

- P-value Calculator — from z, t, or Chi-Square

- The Best Grade 6 ELA Practice Tests for Minnesota Students

- FREE SSAT Upper Level Math Practice Test

- Free Kentucky KSA Grade 5 Math Worksheets: 49 Printable PDFs with Friendly Answer Keys

- 4th Grade SC Ready Math Worksheets: FREE & Printable

- Best Note-Taking Tablet for College Students

- The Practical Benefits Of Knowing Math – The 10 Best Industries For Math Geeks

- 49 Free Grade 3 Math Worksheets for Connecticut SBAC Prep, Built Around the Real Skill List

What people say about "How to Plan and Save for College? (+FREE Worksheet!) - Effortless Math"?

No one replied yet.